Where Is the Aging Housing Stock in the United States?

By Sijie Li, Freddie Mac, Housing Insight and Solutions

- Mike Maciag “The Implications of Older Housing Stock for Cities”

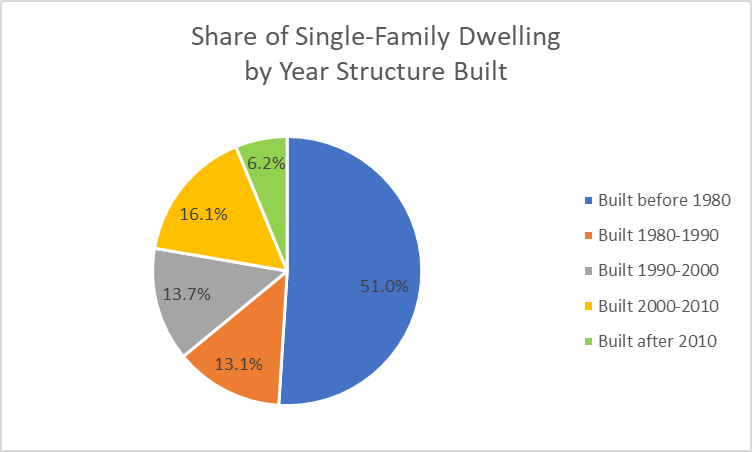

An older housing stock, if not well-maintained, is associated with issues such as energy efficiency and the preservation of affordable housing. However, aging housing stock is not a unique concern in Rochester city. It is a pervasive problem throughout the country. As of 2018, nearly 80% of the US single-family dwelling is at least 20 years old and more than half of them were built before 1980 (see Exhibit 1).

Exhibit 1

With the slow recovery of new home construction after the Great Recession, there is an increasing demand in the home remodeling market. In 2019, Trulia surveyed more than 1,300 U.S. homeowners and found that 90 percent of the respondents plan to remodel their home at some point. Researchers from the Joint Center for Housing Studies of Harvard University found that homeowners spent 50 percent more on remodeling in 2017 than they did at the end of the Great Recession in 2010. These changes in the remodeling activities could be further fueled by the coronavirus pandemic. COVID-19 has led to disruption in new construction inducing severe shortage of new housing stock. Furthermore, future rebound remains uncertain, especially if the economy shuts down again. Affordable housing preservation products such as Freddie Mac’s CHOICERenovation® offer future borrowers the opportunity to purchase an older home and renovate it, rather than waiting for a more expensive newer housing option. In this article, we try to better understand where the aging housing stock is in the United States.

We examine the share of aging housing stock with various geographical focus. Aging housing stock is defined as those houses built before 1980. However, we acknowledge that a home’s construction year does not necessarily reflect its condition. Old houses in the desirable neighborhoods could have already gone through major renovations. We use 1980 as a cutoff for the year structure built because the modern building codes, which require compartmentalization of structures and smoke alarms, took effect during the 1970s and by 1980, these regulations were uniformly implemented to standardize building practice (Barry, 2011).

Existing studies have mainly used the American Community Survey (ACS) by the U.S. census to study the age of housing in the United States. While ACS contains the structure year-built information, it does not record the property type. Moreover, the lowest level of geography in the ACS is Public Use Microdata Areas (PUMAs) where each PUMA contains at least 100,000 people. The data we used in this article comes from the 2018 First American tax records. This dataset allows us to differentiate the building types and therefore, we can focus only on the properties that are related to our Single-Family business. Specifically, we restrict the property types to be single-family houses, townhomes, condominium, planned unit development, and manufactured housing. The overall sample size is greater than 75 million[1]. The dataset also allows us to study the aging housing stock at the census tract level. Census tracts are small, relatively permanent statistical subdivisions of a county that generally have a population size of 4,000 people.

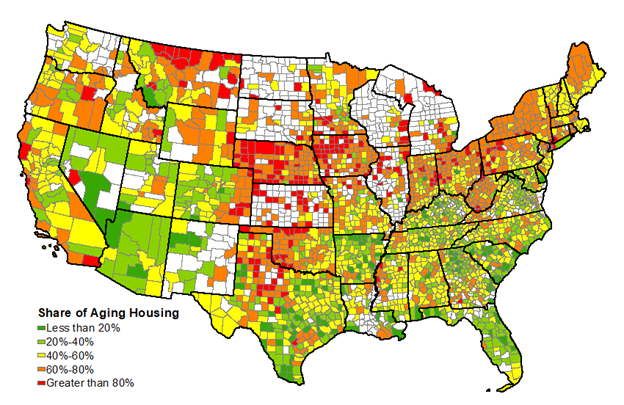

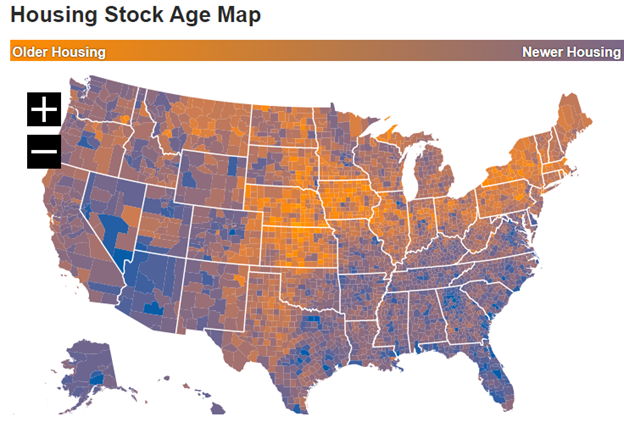

The share of aging housing stock varies greatly by region, with some areas having a particularly large number of older homes. For example, we can see in Exhibit 2 that most counties in the Rust Belt and the Great Plains have shares of aging housing stock greater than 60%. Decades of population decline as young families moved to the urban areas for job opportunities have distorted the age distribution in many of these counties (Rathge, 2001). Older homes may pose more challenges for the older generations. In these places, there is a division of views on whether the older homes should be updated or torn down and replaced. High-cost urban areas such as the west coast counties also have higher share of aging housing stock. In these places, remodeling and renovation could be a better option for homeowners of older homes as the house price in the area continue to rise.

Exhibit 2: Percentage of Single-Family Dwelling Units Built Before 1980 by County

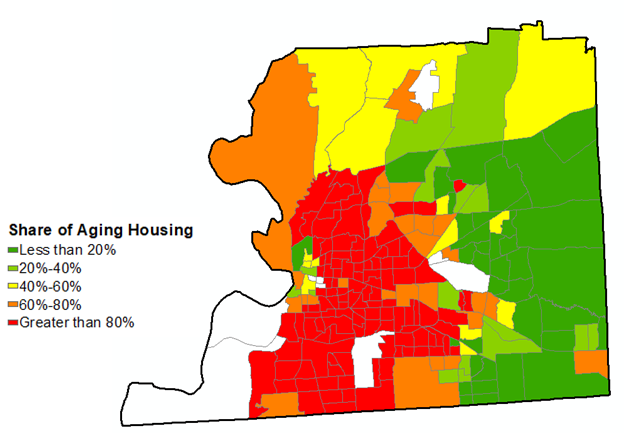

While the overall housing stock looks younger in some areas at the county level, the share of aging housing stock is exponentially higher in selected pockets of the neighborhoods when we examine the data at a more refined geographic level. Exhibit 3 shows an example of the Shelby county, Tennessee at the census tract level[2]. Shelby county is where Memphis city is located, and the overall share of aging housing stock is less than 60%[3]. However, we see that overwhelming majority of the census tracts in the city center have shares of aging housing greater than 80%. Since different census tracts have similar number of residents by default, the spatial size of census tract reveals the density of settlement. We can see from Exhibit 3 that the census tracts in the city center are relatively smaller in size. New residential development may be restricted in these higher-density areas due to zoning codes and ordinances.

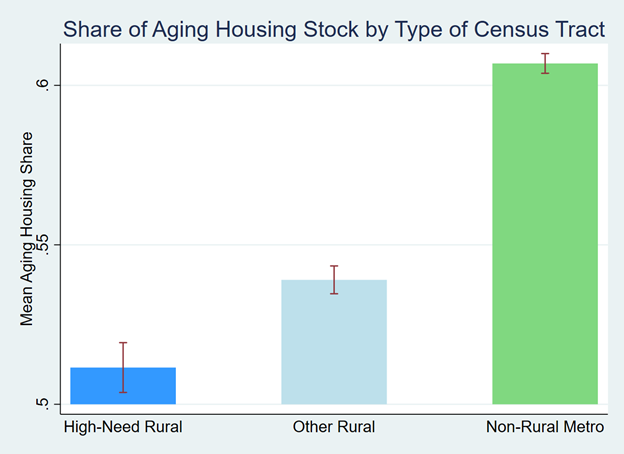

Indeed, Exhibit 4 shows that census tracts in the non-rural metropolitan areas have the highest share of aging housing stock. In contrast, census tracts in the rural areas with more permissive density zoning regimes have lower share of aging housing stock.

Exhibit 3: Shelby County, Tennessee

Exhibit 4: United States

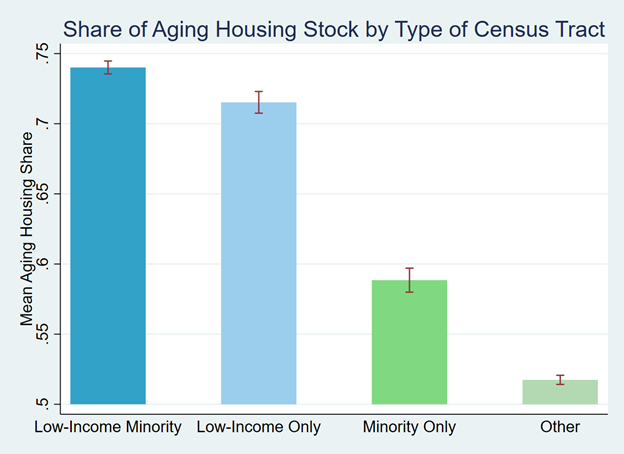

One data limitation is that we cannot observe who are the ones occupying the older homes. However, we can gain some insights by examining the relationship between the share of aging housing stock and the demographic as well as the socioeconomic characteristics at the census tract level. In Exhibit 5, we continue to use Shelby county as an example and indicate the minority tract by the blue diamond label on the left panel, and the low-income tract by the black circle label on the right panel[4]. There is a significant overlap between the minority tracts and the low-income tracts in Memphis. Almost all the census tracts that have more than 80% of their housing stock built before 1980 are the low-income minority tracts. The same observation basically holds true at the country aggregation. As shown in Exhibit 6, low-income minority tracts have the highest aging housing share among all types (74.0%), followed by low-income only tracts (71.5%), minority only tracts (58.8%), and other (51.7%).

In general, low-income and minority families have less housing options because of their lower mobility. As the homes they occupy continue to age, repairing becomes increasingly needed. Even though we cannot confirm whether these old homes have been remodeled, they probably have not been because most of the residents are already financially burdened. Efforts to make homeownership accessible and sustainable to low-income people and minorities are needed. Encouraging renovations in the low-income and minority tracts will not only improve the quality of living of its residents, but also help creditworthy borrowers to build wealth in the housing market.

Exhibit 5: Minority Tract (Left Panel) vs. Low-Income Tract (Right Panel) in Shelby County, Tennessee

-vs.-low-income-tract-(right-panel)-in-shelby-county,-tennessee.png)

Exhibit 6: United States

To sum up, the aging housing stock in the United States has mainly concentrated in the Great Plains and the Rust Belt. Aside from these two regions, non-rural metropolitan tracts also have significantly high shares of aging housing stock. Many of these tracts are low-income and minority tracts. For the reasons we have discussed above, potential borrowers of renovation mortgage products from different areas might have different wealth and demand. By providing innovative financing options for different borrower segments, Freddie Mac can be a part of the solutions to our country’s growing aging housing stock and allow communities to reap the benefits for years to come.

Footnotes

[1] We restrict the sample to houses built after 1900 and having no more than 10 bedrooms.

[2] The spatial size of census tracts varies widely depending on the density of settlement.

[3] The reason we use Shelby county as an example in this article is not because it is a representative county in the United States, but because it is part of our Innovation in Housing markets (see more details in the Appendix).

[4] The Federal Housing Enterprises Financial Safety and Soundness Act of 1992 defines “low-income area” as: (a) census tracts or block numbering areas in which the median income does not exceed 80 percent of area median income (AMI), (b) families with income not greater than 100 percent of AMI who reside in minority census tracts, and (c) families with income not greater than 100 percent of AMI who reside in designated disaster areas. A “minority census tract” is a census tract that has a minority population of at least 30 percent and a median income of less than 100 percent of AMI.

Reference

Barry, N. A. (2011). Determining a community retrofit strategy for the aging housing stock using utility and assessor data.

Joint Center for Housing Studies of Harvard University. (2019). Improving America's Housing 2019.

Maciag, M. (2014). The Implications of Older Housing Stock for Cities. Retrieved from Governing the Future of States and Localities: https://www.governing.com/topics/urban/gov-cities-old-housing-stock.html

Ramirez, K. (2018). Retrieved from https://www.housingwire.com/articles/46427-housing-stock-age-shows-desperate-need-for-new-construction/

Rathge, R. W. (2001). The changing population profile of the Great Plains. . North Dakota State Data Center, North Dakota State University.

Remodeling on the Rise. (2019). Retrieved from Trulia Research: https://www.trulia.com/research/remodeling-on-the-rise/

Zhao, N. (2017). NAHB Eye On Housing. Retrieved from The Aging Housing Stock: http://eyeonhousing.org/2017/01/the-aging-housing-stock-3/

Appendix

To provide some validity checks on the First American tax records, Exhibit 7 shows the average age of housing stock by county in the United States. The data is based on 2014 5-Year American Community Survey. Consistent with our findings, the Great Plain and the Rust Belt are all shaded in orange color (i.e., older housing).

Exhibit 7

Aging Housing Stock in the Innovation in Housing (InH) Markets

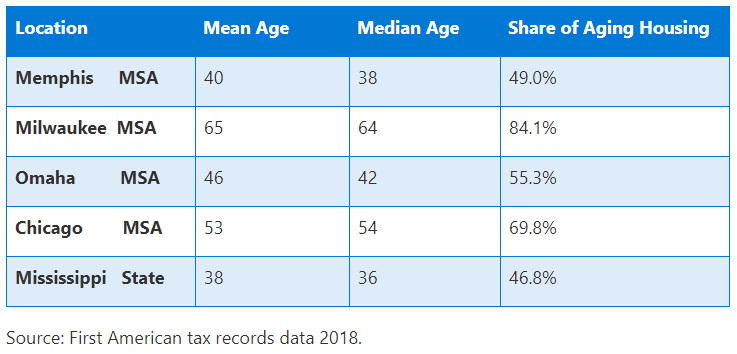

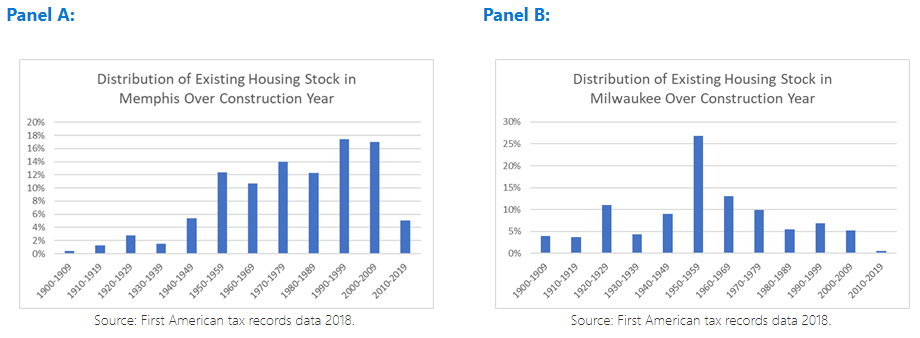

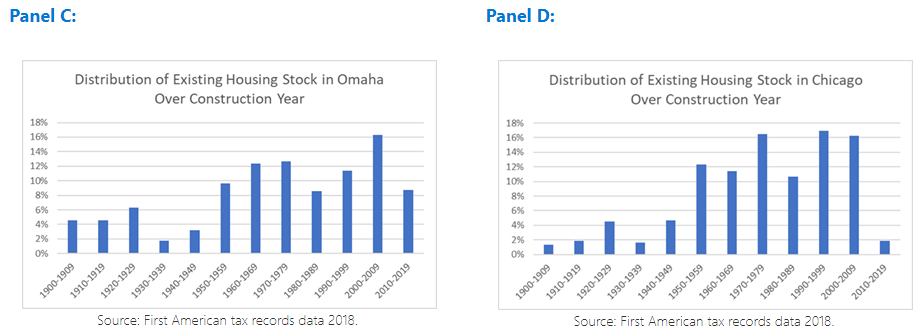

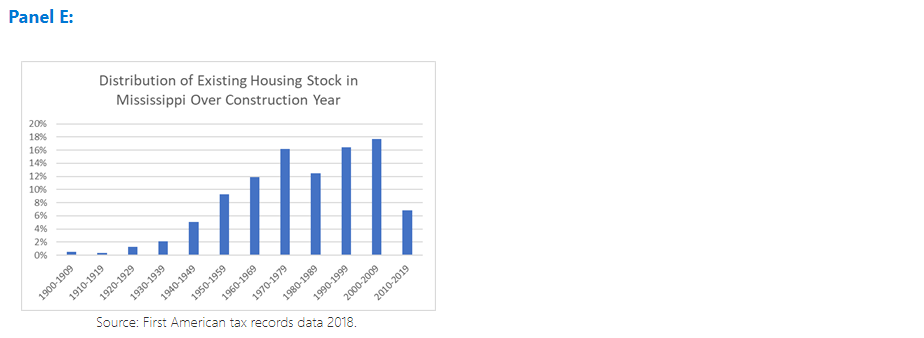

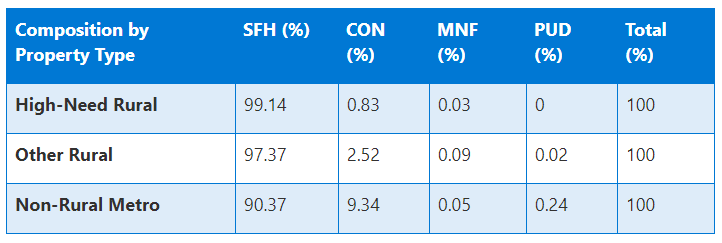

The InH markets consist of four metropolitan areas and one state. They are Memphis, Milwaukee, Omaha, Chicago, and Mississippi. Among all, Milwaukee metropolitan areas have the oldest housing stock. More than 80% of its housing units in 2018 are built before 1980 (see Exhibit 8). Exhibit 9 Panel B shows that majority of them were built in the 1950s. Compared to the rest of the InH markets, we do not see many new constructions in Milwaukee after 1980.

Exhibit 8

Exhibit 9

Aging Housing Stock in the High-Need Rural Tracts

In Exhibit 4, we see that the aging housing share in high-need rural tracts is much smaller than the shares in the other rural tracts and non-rural metro tracts. It is intuitive to understand why the non-rural metro tracts have the highest aging housing shares: they have more stringent zoning restrictions and vintage older houses. However, it is surprising to see high-need rural tracts have lower share of older homes than the other rural tracts. Our prior is that high-need rural tracts should have more aging housing stock due to poverty. Therefore, we take a further examination into our data.

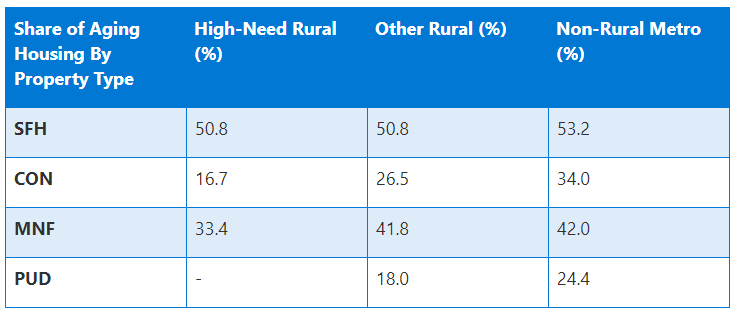

First, we look at the composition of property types by different census tract categories. As shown in Exhibit 10, more than 99% of the single-family dwelling in the high-need rural tracts are single-family homes. They have very low shares of Condominium (CON) and Manufactured Housing (MNF) compared to other rural and non-rural metro tracts. They also have no Planned Unit Development (PUD).

Exhibit 10

Source: First American tax records data 2018.

We then look at the share of aging housing by property type at each category of census tract (see Exhibit 11). We found that the share of single-family homes built before 1980 in high-need rural tracts is the same as the share of single-family homes built before 1980 in other rural tracts. It is the Condominium and Manufactured Housing in the high-need rural tracts that are younger than their counterparts in the other rural tracts.

Exhibit 11

Source: First American tax records data 2018.

It is possible that the Manufactured Housing built in the higher poverty areas are in lower quality and as a result, they will need to be replaced frequently. Also, the higher-density housing development in the high-need rural areas is lagging behind the other areas since they were primarily agricultural when the other cities were being established. As the population increased in recent years, some of the agricultural land may have been converted for higher-density housing. All these reasons above could explain why we see a lower share of aging housing stock in the high-need rural tracts.