Uniform Closing Dataset FAQ

Disclaimer

The information on this page is not part of, and is not a replacement or substitute for, the requirements found in the Freddie Mac Single-Family Seller/Servicer Guide and your other Purchase Documents.

Updated April 2, 2026

Freddie Mac UCD FAQs

The following provides answers to questions frequently asked about Freddie Mac’s and Fannie Mae’s (GSEs’) jointly developed Uniform Closing Dataset (UCD). The GSEs developed the UCD at the direction of the Federal Housing Finance Agency (FHFA) as part of the Uniform Mortgage Data Program® (UMDP®), an ongoing initiative to enhance loan data quality and consistency through uniform data standards for the single-family loans the GSEs purchase.

The GSEs have compiled some of the most common UCD questions below. Questions are grouped by topic: General, Loan Delivery, Embedding the Closing Disclosure PDF in the UCD XML File, UCD Critical Edits, Fees, UCD File Content, Qualified Mortgages and XML File Technical Considerations.

General

What is the Uniform Closing Dataset (UCD)?

The UCD is a common industry dataset allowing information on the Closing Disclosure (CD) to be communicated electronically in a standardized format. The UCD was developed and is maintained by the GSEs and is published on each GSE’s UCD webpage as UCD v1.5 and UCD v2.0 Specifications.

- Helps enhance credit risk management with more data and better-quality data.

- Provides important information to help increase our ability to detect fraud and misrepresentation at loan delivery.

- Lends additional transparency into the mortgage loan transaction file to help assess whether the loan, as closed, meets the GSE’s eligibility requirements.

Is the UCD Specification the same for both GSEs?

Yes. Although the GSEs have implemented separate UCD collection solutions, both GSEs adhere to the guiding principles established under UMDP and are using the identical UCD Specification containing the same data points, enumerations, and conditionalities.

What data do the GSEs collect using the UCD?

The data collected by the UCD includes, in MISMO v3.3.0299 schema order:

- Data points supporting the CD form field data required by both GSEs. (Note that while UCD v1.5 specification (UCD v1.5) contains all data points supporting the entire CD, UCD v2.0 specification (UCD v2.0) contains only data actively used and required by the GSEs.)

- Additional closing transaction supporting data points required to meet GSE business needs, for example: Qualified Mortgage (QM) data.

- Data points needed to properly create the UCD XML file.

- Data points enabling a PDF version of the CD to be embedded in the UCD XML file.

How do the GSEs collect the UCD?

The GSEs have separate collection solution applications for UCD XML file submissions by Sellers. Support and training resources related to each unique collection solution are available on each GSE’s respective UCD webpages, FreddieMac.com and FannieMae.com. Resources to assist with the transition to UCD v2.0 are also available.

What resources are available to help me implement the UCD or update the UCD based on new requirements?

The GSEs have published several jointly developed and maintained implementation materials and artifacts on their respective FreddieMac.com and FannieMae.com websites to assist you with your UCD implementation. It is good practice to visit these websites frequently to ensure you are using the most up-to-date specifications and resources.

Loan Delivery

How does the UCD relate to loan delivery requirements?

The UCD in the XML file format with the Closing Disclosure PDF (CD PDF) embedded must be successfully submitted prior to loan delivery. Every loan purchased by the GSEs requires a UCD submission.

Loans submitted to a GSE’s Selling/Loan Delivery solutions without a corresponding UCD XML file will receive a critical/fatal edit and will not be eligible for purchase until the properly formed UCD XML file including the embedded CD PDF has been received.

Which version of the UCD Specification should I be using for production deliveries? [UPDATED]

The GSEs published the UCD v2.0 in September 2024 to provide a glide path for industry to adopt the new format and requirements within their systems and processes. The UCD v2.0 transition period began on September 29, 2025. Each GSE’s UCD collection solution will accept UCD XML files based on EITHER UCD v2.0 OR v1.5 during the transition. The GSEs will continue to accept UCD XML files based on UCD v1.5 until the UCD v2.0 mandate date. On or after the mandate, all UCD XML files (even files previously submitted based on UCD v1.5) must use UCD v2.0.

IMPORTANT: Submitted UCD XML files based on v1.5 may NOT include any new UCD v2.0 data points or enumerations (including the ucd:FEE_DETAIL_EXTENSION structure), or the file will receive a Specification Version critical/fatal edit.

Can my UCD XML files include any “extra” data that is not included in the UCD Specifications?

Yes. However, the GSEs strongly advise against delivering non-specified data in the UCD XML files. If additional data is included in the UCD XML file, but the file is properly formed according to MISMO v3.3.0, the file will not fail. The GSEs will ignore any data in the UCD XML file not expected per the UCD v2.0.

What is the relationship between data on the UCD and the information on the CD?

Data provided in the UCD XML file must reflect disclosures on the CD PDF as closely as possible. The GSEs understand there may not be a 100 percent match because the CD is often rendered with the values provided in the @DisplayLabelText attribute, while the UCD XML file must include the valid associated enumeration. (See FAQ in XML File Technical Considerations section.)

Do the GSEs provide testing environments for their UCD collection solutions?

Yes, each GSE has established a customer test environment (CTE) that can be accessed by Sellers and software providers/Technology Service Providers (TSPs). Additional details can be found on each GSE’s UCD webpage on FreddieMac.com and FannieMae.com.

Embedding the Closing Disclosure PDF in the UCD XML File

What are the requirements for embedding the CD PDF in the UCD XML file?

- Timing/Version: The CD PDF in the UCD XML file should represent the most accurate, agreed-upon terms of the loan at time of submission of the UCD and Uniform Loan Delivery Dataset (ULDD) XML files to the GSEs. If, after closing, but before acquisition of the loan by the GSEs, information was updated, the most recent UCD data and embedded CD must be provided in the UCD XML file.

- CD Copy: The PDF does not need to be a first-generation file; however, the CD must be clear and legible.

- Simultaneous Seconds: For transactions with loans having a simultaneous second (such as an 80/10/10 transaction), the lender should embed only the copy of CD for the loan being purchased (the subject loan).

- Construction-to-Permanent Loans: The GSEs purchase only the permanent financing portion of a construction-to-permanent loans. Refer to Freddie Mac’s Single-Family Seller Guide and Fannie Mae’s Selling Guide.

- CD Revised Prior to Delivery: If the loan has closed, but has not been delivered to a GSE, and a revised CD was provided to the borrower, the most recent version of the CD must be included in the updated UCD XML file submission.

- Split Disclosures: When separate CDs are provided to the borrower and a Seller, the Seller’s CD is not required in the UCD XML file.

- Addenda: Addendum PDFs that are not associated with the CD do not need to be included in the UCD XML file. However, when an addendum is used to provide additional required information to the CD, all data on the addendum must be included in the UCD XML file, with an IntegratedDisclosureSectionType value reflecting the section being extended by the addendum.

- Signatures: The CD PDF included in the UCD XML file does not need to be signed; however, the Seller may wish to follow industry best practices and obtain interested party signatures.

What is the Alternate Form for Transactions Not Involving a Seller?

The Alternate Form (Regulation Z Model Form H-25(J)) provides a safe harbor model Closing Disclosure that can be provided for transactions that do not involve Sellers, including refinance transactions. The form is abbreviated to omit data that only applies to purchase transactions. If the Alternate Form is provided to the borrower, the corresponding CD PDF must be embedded in the UCD XML file.

May the Model Form be used for Refinance Transactions?

Yes. Although the GSEs prefer that the lender take advantage of the shorter Alternate Form for refinance transactions, the CD Model Form (Regulation Z Model Form H-25(A)) may be used for refinance transactions.

UCD Critical Edits

What is the UCD Critical Edits transition?

The GSEs are converting certain data edits in their CD collection solutions from “warning/warning-to-fatal” to “critical/fatal”. The multi-year rollout approach, now in its fourth phase, enforces the UCD Specification conditionality details for selected data points. The enforcement of critical/fatal edits is designed to enhance data quality and consistency for the single-family loans purchased by the GSEs.

How do we prepare for the latest UCD Critical Edits? [UPDATED]

The GSEs recommend preparing for the Phase 3B Postponed and Phase 4 UCD Critical Edits by referring to the resources, including the UCD Critical Edits Matrices, that are available on the GSEs’ UCD webpage, FreddieMac.com and FannieMae.com. Critical edits enforce the conditionality details provided in the UCD v2.0 Specification, which is the best source for preparation.

What value is expected in the GSE-Specific Data Point LoanPriceQuoteInterestRatePercent? [UPDATED]

The MISMO v3.3.0 Logical Data Dictionary definition for this data point is: “The mortgage loan interest rate for which the price quote is calculated.” To ensure the correct rate is delivered in this data point, refer to the Loan Price Quote Interest Rate Percent Job Aid on the GSEs’ UCD pages on their respective websites.

Are the Phase 3B Postponed and Phase 4 edits supported by the UCD v2.0 requirements?

Yes. If you fully comply with the cardinality and conditionality specified in UCD v2.0, you will meet all critical edit requirements. Datapoints under critical edits are identified on Tab 7-UCD v2.0 XML Requirements in column N “Critical Edit Matrix Phase”.

How do we handle loans in our closing system pipeline during the transition to the mandate dates?

There is no need to manage pipeline loans in the GSE’s UCD collection solutions. Submissions must cut over to UCD v2.0 and the associated edits will be in effect as of the mandate date. UCD XML files submitted before the mandate may be in either the UCD v1.5 or UCD v2.0 format, and after the mandate must be v2.0 (even if resubmitting a loan previously submitted in v1.5 format).

What do I provide in the UCD XML file when a fee cannot reasonably be mapped to a UCD v1.5 FeeType or UCD v2.0 ucd:FeeItemType supported enumeration?

You must provide FeeType / ucd:FeeItemType = “Other” and FeeTypeOtherDescription / ucd:FeeItemTypeOtherDescription only when an enumeration that reasonably reflects the fee is not supported by the UCD Specification version. Seventy-three enumerations were added in UCD v2.0 for ucd:FeeItemType. See Tab 9- FeeItemType Enumerations in UCD v2.0 for these new values.

Will I receive an error message if I send a UCD supported enumeration for ucd:FeeItemTypeOtherDescription or FeeTypeOtherDescription?

There are situations when using ucd:FeeItemTypeOtherDescription or FeeTypeOtherDescription is warranted, e.g., for specialized or jurisdiction specific charges, but if a UCD-supported enumeration reasonably represents the disclosure of fees on the CD it must be used in the UCD XML file. The GSEs are monitoring the use of ucd:FeeItemType = ‘Other’ plus ucd:FeeItemTypeOtherDescription for content and frequency; however, no critical edits are currently planned when the use of ‘Other’ exceeds a certain number within the UCD XML file. Lender-level usage reports can be made available upon request to your Freddie Mac or Fannie Mae account representative.

Can I use the UCD Production Schema to validate the XML for UCD v1.5 or earlier datasets that I exchange with non-GSE trading partners? [NEW]

No. The UCD v2.0 Production Schema should not be used to validate UCD v1.5 or earlier XML files you exchange with other trading partners. The UCD v2.0 Production Schema is tailored to the GSE data requirements reflected in the UCD v2.0 and does not support CD fields that support loan products the GSEs do not buy.

Fees

How should recording fees and amounts be included in UCD v1.5 FeeType / UCD v2.0 ucd:FeeItemType = “Recording Fee Total”? [UPDATED]

The value provided for FeeType (v1.5) / ucd:FeeItemType (v2.0) = “RecordingFeeTotal” should be the sum of the amounts of all recording fees paid or to be paid to any government authority, regardless of the entity collecting the payments. This sum must also include the amounts for FeeType (v1.5) / ucd:FeeItemType (v2.0) = “RecordingFeeForMortgage” and “RecordingFeeForDeed.” Include the following data points for Recording Fee Total (and any other non-mortgage or non-deed recording fee line items) according the applicable UCD Specifications:

UCD v1.5 | UCD v2.0 |

|---|---|

| FEE_DETAIL Integrated Disclosure Section Type = “TaxesAndOtherGovernmentFees” FeeType = “RecordingFeeTotal” @DisplayLabelText FEE_PAYMENTS FEE_PAYMENT FeeActualPayment Amount FeePaymentPaidByType FeePaymentPaidOutsideOfClosingIndicator | FEE_DETAIL Integrated Disclosure Section Type = “TaxesAndOtherGovernmentFees” EXTENSION OTHER ucd:FEE_DETAIL_EXTNESION ucd:FeeItemType = “RecordingFeeTotal” @DisplayLabelText FEE_PAYMENTS FEE_PAYMENT FeeActualPayment Amount FeePaymentPaidByType FeePaymentPaidOutsideOfClosingIndicator |

Refer to the UCD Phase 3 Critical Edits Job Aid: Taxes and Other Government Fees on the GSEs’ UCD webpages FreddieMac.com and FannieMae.com for more information.

Do we need to include the fees for “LoanDiscountPoints”, “PrepaidInterest” and “LenderCredits” in the UCD XML file even when they are not part of the loan transaction?

Yes, these data points must be provided in the UCD XML file as described:

- Even when discount points are not part of the transaction, UCD v1.5 FeeType or UCD v2.0 ucd:FeeItemType = “LoanDiscountPoints” along with FeeActualPaymentAmount value equal to “0.00” are required for all loans and must be provided in the UCD XML file. FeeTotalPercent is not required when FeeActualPaymentAmount is “0.00”.

- Even when prepaid interest is not part of the transaction, UCD v1.5 and v2.0 PrepaidItemType = “PrepaidInterest” along with PrepaidItemActualPaymentAmount = “0.00” must be provided in the UCD XML file.

- Even when lender credits are not part of the transaction, UCD v1.5 and v2.0 IntegratedDisclosureSubsectionType = “LenderCredits” along with IntegratedDisclosureSubsectionPaymentAmount = “0.00” must be provided in the UCD XML file.

How will the Phase 3B Postponed critical edits enforce the section required for a given fee?

In 2024, the GSEs removed the Phase 3B critical edits enforcing a limited set of fee enumerations allowed with IntegratedDisclosureSectionType = ‘BorrowerDidShopFor’, ‘BorrowerDidNotShopFor’, and ‘Other’.

In UCD v2.0, any supported ucd:FeeItemType enumeration may be used in those sections. Supported enumerations for IntegratedDisclosureSectionType = ‘OriginationCharges‘ and ‘TaxesAndOtherGovernmentFees’ are limited and have been published in the UCD v2.0 Specification and the UCD v2.0 Critical Edits Matrix. See Tab 9-FeeItemType Enumerations in UCD v2.0 for those subsets.

In UCD v2.0, how do we deliver enumerations that were specified for certain “OtherDescription” data points in UCD v1.5? [UPDATED]

In UCD v1.5, the following data points ending in “OtherDescription” specified the following enumerated values:

- UCD Unique ID 10.141 - ClosingAdjustmentItemTypeOtherDescription = “PrincipalReduction | SellersReserveAccountAssumption”

- UCD Unique ID 8.169 - EscrowItemTypeOtherDescription = “BoroughPropertyTax”

- UCD Unique ID 15.015 - FeeTypeOtherDescription = “DebtSuspensionInsurancePremium” (This example is valid for UCD v1.5; for v2.0 use ucd:FeeItemType = “DebtSuspensionInsurancePremium”)

- UCD Unique ID 10.205 & 10.234 - ProrationItemTypeOtherDescription = “OtherAssessments”

UCD v2.0 treats these data points as strings and does not validate the values provided. The values formerly specified as enumerations for these data points may still be provided as string fields (as may any other non-UCD supported enumeration). Should any of these apply to the transaction, provide the text string in the same format shown in UCD v1.5.

UCD XML File Content

When the Alternate Form is used for a refinance transaction, how should any gifts or grants be provided in the UCD XML file?

The required data points when the Alternate Form is used are listed below with the UCD v1.5 UID, a slash, then the UCD v2.0 UID:

- 16.016 / 10.039 ClosingAdjustmentItemAmount

- 16.024 / 10.211 ClosingAdjustmentItemPaidOutsideOfClosingIndicator

- 16.017 / 10.042 ClosingAdjustmentItemType = “Gift” or “Grant”

- 16.020 (same in both specification versions) IntegratedDisclosureSectionType = “PayoffsAndPayments”

- 16.023 /10.308 FullName with the full name of the individual providing the gift, OR

- 16.022 / 10.043 FullName with the full, unparsed name of the legal entity providing the grant.

- 16.021 (same in both specification versions) gse:FullName with the full, unparsed name of the payee

When the Model Form is used for a refinance transaction, the data points to be provided in the UCD XML file are the same, with the following substitutions for the Model Form heading and subheading:

- 10.162 (same in both specification versions) IntegratedDisclosureSectionType = “PaidAlreadyByOrOnBehalfOfBorrowerAtClosing”

- UID 10.163 (same in both specification versions) IntegratedDisclosureSubsectionType = “OtherCredits”

When should Mortgage Broker and Real Estate Agent contact information be provided in the UCD XML file? [NEW]

Complete contact data points as documented in the UCD v2.0 must be provided for each party participating in the closing transaction. Parties should be left blank where no such person is participating in the transaction. Phase 4 critical edits will enforce the presence of Mortgage Broker and Real Estate Agent(s) if fees for their services are included in the UCD XML file.

I have run my loan through both Desktop Underwriter® (DU®) and Loan Product Advisor®(LPA®) and received an Automated Underwriting Case Identifier from both systems. Can I include the Automated .....

Question: I have run my loan through both Desktop Underwriter® (DU®) and Loan Product Advisor® (LPA®) and received an Automated Underwriting Case Identifier from both systems. Can I include the Automated Underwriting Case Identifier and Automated Underwriting Case System Type for both DU and LPA in the same UCD XML file?

Answer: Yes. You may include two instances of Automated Underwriting Case Identifier and Automated Underwriting System Type in the UCD XML file:

One with Automated Underwriting System Type = “DesktopUnderwriter” and second instance with Automated Underwriting System Type = “Other” / Automated Underwriting System Type OtherDescription = “LoanProductAdvisor”.

In the UCD v2.0 Specification Purchase Credit line item – ClosingAdjustmentItemType references “TradeEquity” as an enumeration. It appears that “TradeEquityPropertySwap” is supported in MISMO v3.4 and later versions of the ....

Question: In the UCD v2.0 Specification Purchase Credit line item – ClosingAdjustmentItemType references “TradeEquity” as an enumeration. It appears that “TradeEquityPropertySwap” is supported in MISMO v3.4 and later versions of the reference model. Can we use “TradeEquityPropertySwap” in lieu of “TradeEquity”? [NEW]

Answer: As UCD is based on MISMO v3.3, the 'TradeEquity' enumeration must be used for ClosingAdjustmentItemType and “TradeEquityPropertySwap” is not accepted.

How do I determine the value that should be delivered UID 4.039 Average Prime Offer Rate Percent (APOR)?

Refer to https://ffiec.cfpb.gov/tools/rate-spread for information on how to calculate the APOR.

How do I identify in the UCD file fees related to a loan with a temporary buydown?

If the loan has a temporary buydown feature, include the following data points in the UCD XML file:

- Buydown Temporary Subsidy Funding Indicator = “true”

- Fee Type = “TemporaryBuydownPoints” (the total dollar amount of the buydown fund)

- Fee Type = “TemporaryBuydownAdministrationFee” (the total cost to the borrower for the service of establishing the buydown fund, when charged)

What value is expected in UID 3.038 Current Rate Set Date?

As defined in the MISMO v3.3.0 Logical Data Dictionary and reflected in the UCD Specifications, Current Rate Set Date is, “The date on which the interest rate for the loan was set by the lender for the final time before closing.”

How do I indicate that that the Secured Overnight Financing Rate (SOFR) was used as the index for an Adjustable-Rate Mortgage (ARM) Transaction?

The value “Other” should be provided in Unique ID 11.055 Index Type and the value “SOFR” should be provided in Unique ID 11.100 Index Type Other Description.

Note: If your business process requires delivery of ‘30DayAverageSOFR’, this value can be delivered in the UCD XML file instead of ‘SOFR’ and will not impact the status of your UCD submission or the eligibility of the loan.

How is the subject property address provided when it does not have a street address (for example, for construction loans)?

Provide Unique ID 1.012 Unparsed Legal Description along with Unique ID 1.011 Postal Code.

What UCD values for ConstructionMethodType do we use in our AUS (automated underwriting system)?

The MISMO versions supporting our AUSs, UCD and ULDD accommodate a single ConstructionMethodType per property. The following table provides a mapping from the value reported from the Uniform Appraisal Dataset (UAD) to these datasets when a single ConstructionMethodType is identified.

| Single Value Reported in UAD | Report This Value In | ||

|---|---|---|---|

| DU and LPA | UCD | ULDD | |

| Manufactured | Manufactured | Manufactured | Manufactured |

| OnFrameModular | SiteBuilt | SiteBuilt | SiteBuilt |

| Modular | SiteBuilt | SiteBuilt | SiteBuilt |

| SiteBuilt | SiteBuilt | SiteBuilt | SiteBuilt |

| Container | SiteBuilt | Container | Container |

| ThreeDimensionalPrintingTechnology | SiteBuilt | ThreeDimensionalPrintingTechnology | ThreeDimensionalPrintingTechnology |

When UAD reports multiple ConstructionMethodTypes the following table provides the mapping to the AUSs UCD and ULDD:

| Multiple Values Reported in UAD | Report This Value In | ||

|---|---|---|---|

| DU and LPA | UCD | ULDD | |

| Manufactured and SiteBuilt | Manufactured | Manufactured | Manufactured |

| Manufactured and OnFrameModular | Manufactured | Manufactured | Manufactured |

| Manufactured and Modular | Manufactured | Manufactured | Manufactured |

| Manufactured and Container | Manufactured | Manufactured | Manufactured |

| Manufactured and ThreeDimensionalPrintingTechnology | Manufactured | Manufactured | Manufactured |

| SiteBuilt and OnFrameModular | SiteBuilt | SiteBuilt | SiteBuilt |

| SiteBuilt and Modular | SiteBuilt | SiteBuilt | SiteBuilt |

| SiteBuilt and Container | SiteBuilt | SiteBuilt | SiteBuilt |

| SiteBuilt and ThreeDimensionalPrintingTechnology | SiteBuilt | SiteBuilt | SiteBuilt |

| OnFrameModular and Modular | SiteBuilt | SiteBuilt | SiteBuilt |

| OnFrameModular and Container | SiteBuilt | SiteBuilt | SiteBuilt |

| OnFrameModular and ThreeDimensionalPrintingTechnology | SiteBuilt | SiteBuilt | SiteBuilt |

| Modular and Container | SiteBuilt | SiteBuilt | SiteBuilt |

| Modular and ThreeDimensionalPrintingTechnology | SiteBuilt | SiteBuilt | SiteBuilt |

| Container and ThreeDimensionalPrintingTechnology | SiteBuilt | SiteBuilt | SiteBuilt |

How can I reflect a simultaneous second loan in the UCD XML file? [UPDATED]

If the subject loan includes subordinate financing closing simultaneously, UCD Unique ID 16.015 gse:SubordinateFinancingIsNewIndicator = “true”. If the proceeds of a subordinate lien are part of the transaction as reflected by the presence of ClosingAdjustmentItemType = "ProceedsOfSubordinateLiens" in the UCD XML file, include UCD Unique ID 10.291 TotalSubordinateFinancingAmount. The TotalSubordinateFinancingAmount must report the full principal balance / credit limit of the subordinate financing (e.g., the second mortgage or HELOC), not just the amount applied on the CD.

How do I resolve the edit messages related to the “LoanDeliveryFilePreparer”? [NEW]

This edit message appears when the UCD XML file is missing a value for LoanDeliveryFilePreparerIdentifier, which is required along with PartyRoleType = LoanDeliveryFilePreparer.

To correct this, ensure that the Software Provider ID of the party responsible for preparing the Loan Delivery File is included in the UCD XML file.

- If you are using a vendor solution, contact your vendor directly for assistance.

- If you are using an internal or proprietary system, reach out to your internal support team for guidance.

How do I report Liabilities in the UCD XML file? [NEW]

The following data points must be provided for a complete liability line item, regardless of the CD format used:

- 10.338 LiabilityType / 10.337 LiabilityTypeOtherDescription

- 10.354 @DisplayLabelText (if desired)

- 16.011 gse:LiabilitySecuredBySubjectPropertyIndicator

- 10.350 gse:IntegratedDisclosureSectionType = “DueFromBorrowerAtClosing” (Model form) | 16.012 gse:IntegratedDisclosureSectionType = “PayoffsAndPayments” (Alternate form)

- 10.343 LIABILITY_HOLDER/FullName

- 10.334 PayoffAmount

Qualified Mortgages

The UCD contains several Ability-to-Repay (ATR) data points. Do these data points need to be included in the UCD XML file?

Yes. Even though some of this data is not on the CD, the GSEs require it to be submitted in the UCD XML file.

If a loan is considered exempt from Regulation Z’s ATR requirements, how should this be reflected in the UCD XML file?

The following data points and values should be included in the UCD XML file if the loan is exempt from Regulation Z’s ATR requirements:

- Ability To Repay Method Type = “Exempt”

- Ability To Repay Exemption Reason Type = “PropertyUsage” for ATR exempt investment properties used for business purposes or “LoanProgram” for exempt Housing Finance Agency (HFA) loans

- Refer to Freddie Mac’s Guide Bulletin 2021-19 / Fannie Mae’s Lender Letter LL-2021-11 for policy guidance.

When should the data point gse:QualifiedMortgageShortResetARM_APRPercent be included in the UCD XML file?

gse:QualifiedMortgageShortResetARM_APRPercent is required for all ARMs with an adjustment within five years of the note date.

XML File Technical Considerations

Do the GSEs validate that the submitted UCD XML file formation is correct?

Yes. Upon receipt, each GSE validates the UCD XML file structure and syntax against the MISMO v3.3.0299 Reference Model schema upon submission. For UCD XML files based on the UCD v2.0, the GSEs will also validate against the ucd schema (ucd.xsd).

How should I handle negative values in the UCD XML file? For example, should the Aggregate Adjustment value in the Closing Costs Details section of the Closing Disclosure be submitted as a negative value in the XML file?

In general, any value that is reflected as a negative value on the CD, for example, an aggregate adjustment, should be provided as a negative value in the UCD XML file. Refer to the Potential Sign Conflict table in the UCD Implementation Guide for additional examples.

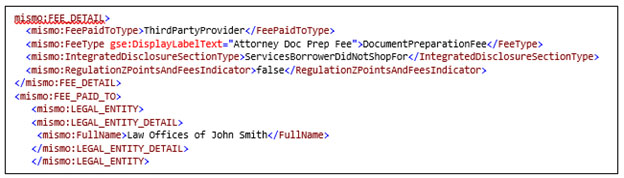

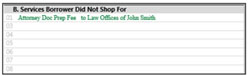

What is the DisplayLabelText attribute?

The DisplayLabelText attribute is used by document preparation providers to render a non-enumerated value on the CD for fee, prepaid, escrow, liability and closing adjustment items. This allows Sellers to continue to use proprietary terminology when disclosing costs. For example, a DisplayLabelText value of “Attorney Doc Prep Fee” appears on the CD, but the corresponding supported enumerated value of “DocumentPreparationFee” would be provided for FeeType (v1.5) / ucd:FeeItemType (v2.0) in the UCD XML file. A sample XML snippet based on UCD v1.5 is provided below:

Sample XML Snippet:

Sample Form Snippet:

Subscription Center

Get and stay connected with Freddie Mac Single-Family. Subscribe to our emails and we'll send the information that you want straight to your email inbox.